Retirement Pensions Are Our #1 Problem (and what you need to know about it)

“It’s not what we don’t know that hurts us, it’s what we know that ain’t so.”

—Will Rogers

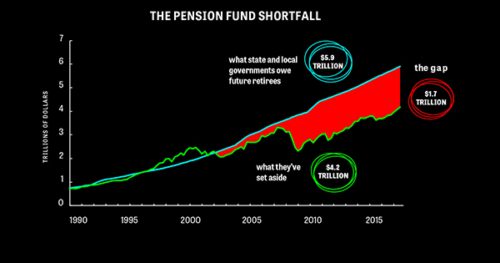

America’s significant retirement pension funds are underfunded by an unfathomable $4.2 Trillion, according to an August 6 Wall Street Journal article. Ventura mirrors this phenomenon. Ventura workers participate in the state pension fund, CalPERS—the largest in the country. CalPERS is only 71% funded as of June 30, 2018, despite a 10-year bull market and a growing economy.

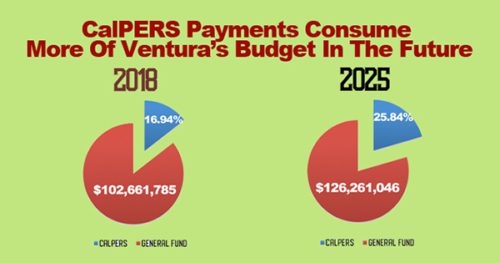

Because of the chronic funding shortfall, CalPERs demands rapidly increasing contributions from all participating local governments. Ventura will have permanent increases of at least $2 million per year for five to six consecutive years.

We respect the work city employees do. There is no denying that fire and police preform a vital job that is both dangerous and requires a high level of training and responsibility. Our concern is not about their work. It’s about the structure by which their retirement is accumulated and paid after retirement.

It is undeniable that city employees’ retirement pensions are crowding out the city’s ability to provide the service itself. Moreover, chronic underfunding of pensions will eventually hit a breaking point jeopardizing benefits too. Something in this equation has to change.

Retirement Pensions Today

Most state, county and local pension benefits are considered to carry a virtually iron-clad guarantee to the workers to whom they have been promised. Even the smallest attempts to alter future benefits—much less  current ones—have been met with furious opposition. Workers’ representatives and also the plan managers themselves—like CalPERS—oppose changes. That opposition has been mostly successful. Governments at all levels are hamstrung between their duties to provide on-going services to their citizens and their ever-increasing financial obligations to pension funds. In the State of California, once one hires an employee, their retirement cannot be changed.

current ones—have been met with furious opposition. Workers’ representatives and also the plan managers themselves—like CalPERS—oppose changes. That opposition has been mostly successful. Governments at all levels are hamstrung between their duties to provide on-going services to their citizens and their ever-increasing financial obligations to pension funds. In the State of California, once one hires an employee, their retirement cannot be changed.

A typical city employee would receive a pension almost the same as his or her working salary if they participated for their whole career. In the case of many public safety employees, their retirement will last longer than their employment as they are fully vested in their retirement pensions by age 50 or 55. For so-called “miscellaneous” employees (all others) the retirement age is higher, usually 62. Nevertheless, the years in retirement can still equal or exceed those worked.

Discussions about pensions get emotional because we’re talking about people’s future and security. What gets lost in the arguments is this. The law and politics guarantee retirement pension benefits, but not the actual returns on investments. There is no separate investment market for pension funds. All investment pools, large and small, invest in the same markets. The myth is that pensions are safe. They are not. The difference is that taxpayers pick up the difference between reality and what politicians promised.

Unprecedented Bull Market

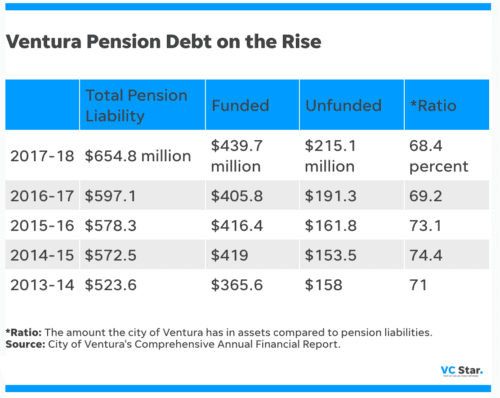

For the past ten years, since mid-2009, there has been an incredible bull market in stocks. CalPERS has posted many good returns during those years. However, Ventura’s pensions are underfunded by $215.1 million. For far too long, pension promises have been at levels far beyond what the real markets can provide.

What Can We Do To Fix Retirement Pensions?

Politicians have made many attempts to improve the current system, but none have addressed the problem in a meaningful way. CalPERS does offer one solution: Cities can buy out of the system—technically—but the costs are so enormous that no municipality can realistically consider that an option. It’s no accident, of course. CalPERS’ onerous payment demand to end participation is designed to be a straight-jacket. As of June 30, 2017, for the City of Ventura, the amount required to get out of CalPERS is $1.254 Billion.

League of California Cities and Government Finance Officers Association recommended actions to confront unsustainable pensions.

- Reduce the unfunded liability by making annual catch-up payment even more than CalPERS instructs you to pay—if you can afford to pay more.

- Raise taxes

- Reduce services

- Require voter approval of any pension obligation bond, or POB.

Pension Obligation Bonds Explained

A city issues a pension obligation bond to pay down the unfunded pension liability. The POB converts the pension liability into a fixed rate of return. There are considerable underwriting costs when issuing a POB. The city invests the money received from the bond into higher returning investments, usually in the stock market. The central idea is that the stock market investments will produce a higher return than the fixed interest rate on the bond, thereby earning money for the pension fund.

A POB creates debt to pay off debt. Such a bond is essentially a gamble with public money. Simi Valley is considering issuing a POB, and Ventura might follow suit if Simi Valley is successful.

The League of California Cities and Financial experts, including Government Finance Officers Association, strongly discourage local agencies from issuing Pension Obligation Bonds (POBs). This approach (going into debt to pay off debt) “only delays and compounds the inevitable financial impacts.”

These are terrible choices for the public.

What The City Council Might Do To Reform Retirement Pensions

There are two other choices for our City Council to consider if they have the political will to do anything about this crisis that will cripple the City of Ventura.

There are two other choices for our City Council to consider if they have the political will to do anything about this crisis that will cripple the City of Ventura.

- Make beneficiaries pay more. With the city covering 100 percent of the unfunded liability, the problem will continue to grow. There will be minimal reforms because the actuarial losses fall on the taxpayer. Capping the employer contribution at a fixed percentage of salary would cut pension costs for the city. As pension costs increase over the years, the employees will pay all the costs associated with the growth.

- Change when retired city employees may begin collecting pensions. This alternative solution applies to new employees only. What if police and fire could fully vest their generous pensions by age 50 or 55, as they do now, but the payments did not start until age 65? Why would that help? The reason is that even if the city makes no further contributions, the fund will have ten more years to grow. At current official pension growth rates, that would more than double the value of that fund over those ten years. Also, the retirement payment period would be ten years shorter, given the same life expectancy. Such a system would still offer retirement security, but it would start at what most of us consider average retirement age.

Public sector employees may resist the changes but think about it. Private sector employees don’t get their full social security until 65 or even 67, depending the year they were born. Moreover, Social Security is only going to be one quarter to one-half of your working earnings.

Public sector employees may resist the changes but think about it. Private sector employees don’t get their full social security until 65 or even 67, depending the year they were born. Moreover, Social Security is only going to be one quarter to one-half of your working earnings.

Editor’s Comments

Even with an unprecedented bull market, Ventura’s unfunded pension liability grew over the past ten years. During such a period, one would expect the excess liability to at least shrink some.

Instead, the pension liability is growing faster than market returns can ever expect to make up. CalPERS annual demand will now permanently increase by about $2 million per year for the five to six years and then stay there. There is no assurance it will not increase even further in the future. Something has to change. Otherwise, the city will either cut back needed services, raise taxes, or both.

Past retirement pension negotiations were based on union bargaining and raw political power, creating a gap between what politicians promised and what cities realistically can pay. We offer some solutions, but it will take political will to bring the retirement benefits back to reality. Changing the system is the only way these promised benefits can be truly sustainable and dependable for retirees. It’s also the only way that taxpayers can afford to pay for them.

Demand Retirement Pension Reform

Below you’ll find the photos of our current City Council. Click on any Councilmember’s photo and you’ll open your email program ready to write directly to that Councilmember.

|

|

|

|

|

|

|

|

|

|

For more information like this, subscribe to our newsletter, Res Publica. Click here to enter your name and email address.